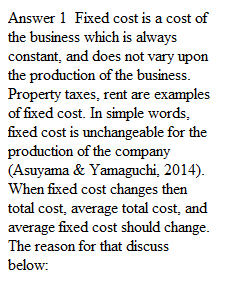

Q Reminder: You may not submit handwritten work in this course, even scanned in work or pictures imbedded in a .doc or .docx file. You need to type all of your work into a .doc or .docx file and submit that file. PDF files are not allowed. 1. When Fixed Cost change, which of the following other costs will change? Explain why you selected the costs you did. Variable Cost Total Cost Average Total Cost Average Variable Cost Average Fixed Cost Marginal Cost 2. When Variable Cost change, which of the following other costs will change? Explain why you selected the costs you did. Fixed Cost Total Cost Average Total Cost Average Variable Cost Average Fixed Cost Marginal Cost 3. What assumption is made concerning short-run production that causes the short-run cost curves to have their typical shapes?

View Related Questions